Georgetown University negotiates its fringe benefit rate annually and its facilities and administration (F&A) rate every three years with DHHS Division of Cost Allocation. The latest University’s Federally Negotiated Indirect Cost Rate Agreement (NICRA) dated January 30, 2023 and should be included in all federal grant and contract proposals.

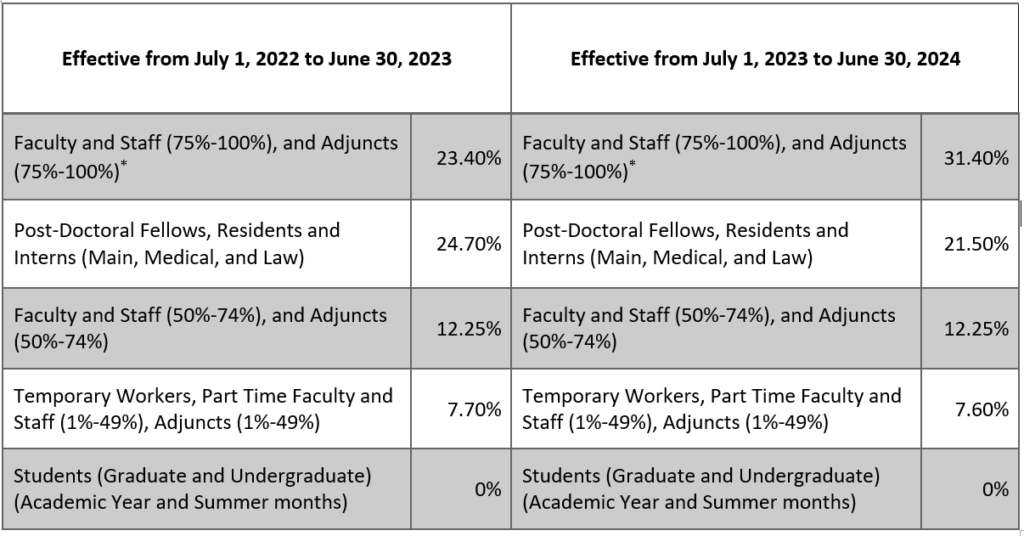

Note 1: When the cumulative Calendar YTD pay for an employee reaches $125K, the fringe rate is reduced by 12%. When it reaches $205K, it is reduced to 0%. These limits are set by the University’s Human Resources Office and by the Executive Committee and are subject to change. Note 2: Fringe Benefit rates are negotiated annually with the cognizant federal agency and thus, cannot change until the next annual negotiations. Therefore, the current fringe benefit rates will continue to be governed by our current NICRA and will not be affected by a temporary situation such as COVID-19.

Indirect costs, otherwise known as Facilities and Administrative, or F&A, rates, are charged on most external research grants. The rates vary depending on the sponsor and other factors, as outlined below.

For proposals submitted to the National Endowment for the Humanities and the National Endowment for the Arts, and in accordance with NEH* and NEA guidelines respectively, the indirect cost (IDC) rate used will depend on the nature of the proposed work. For most proposals for fellowship and stipend awards, and when a zero rate is explicitly required, generally no IDC can be charged. In rare cases the negotiated Federal “Organized Research” rate might apply, but in general it is expected that for research and scholarship typical of the humanities, the “Other Sponsored Activities” IDC rate should be used. Because Georgetown has negotiated Federal rates, a de minimus rate is not applicable. Current negotiated Federal IDC rates can be found here.

* At the NEH link, navigate to Section 11. Budget Revisions, and scroll down to the text following item G for an explanation of allowable IDC rates.

* When a sponsor has a published IDC rate, that rate will be adhered to. When the sponsor does not have a published rate, the University typically charges 30% for pharmaceutical agreements and 15% for foundation / other corporate agreements, although the University will accept the maximum rate that the sponsor is willing to allow. Please provide documentation for the IDC rate you are using as part of the proposal package in GU Pass.

There are exceptions where an IDC reduction or waiver are considered. The PI must request a Vice-Provost of Research approval of this reduction/waiver by email. This approval must be included along with the proposal package routed for internal approval via GU Pass.

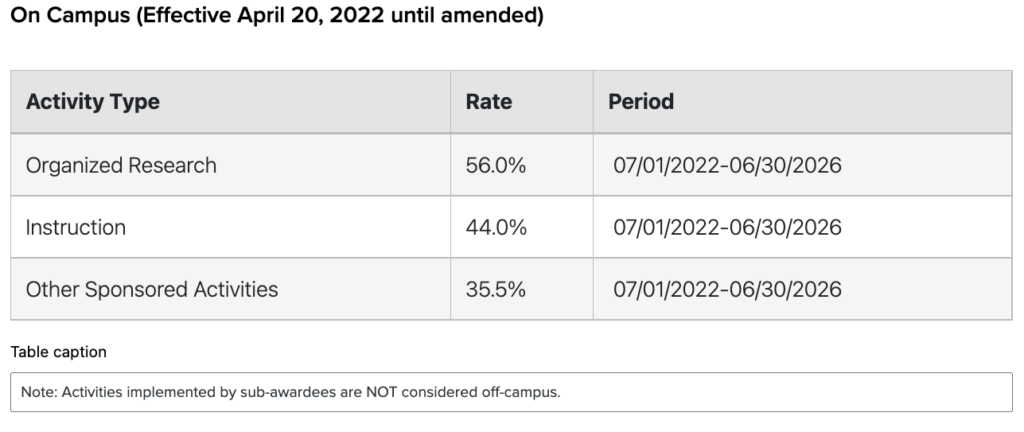

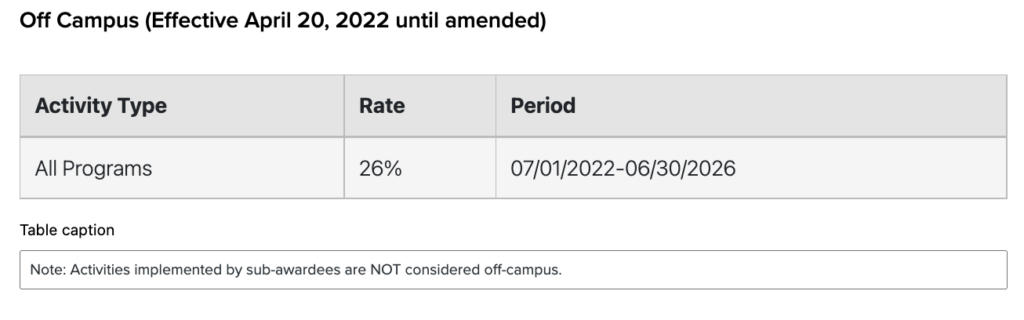

Note that all IDC rates are charged on direct costs. Total costs include both direct and indirect costs, so the share of total costs that goes to indirects is not equal to the IDC rate. In general, if the IDC rate is r, the share of indirects in total costs is r/(1+r). For example, the current Organized Research IDC rate is 56%, so the share of indirects in total costs is 0.56/1.56 = 35.9% when this rate is applied. Similarly, the current Other Sponsored Activities IDC rate is 35.5%, so when this rate is applied, the share of indirects in total costs is 0.355/1.355 = 26.2%.

Calculate indirect cost by multiplying modified total direct cost by the appropriate indirect cost rate. Modified total direct cost is total direct cost minus the cost of the items below.

Alterations/Renovations to office or laboratory space Equipment ($5,000 and over) Patient care Participant costs Rental of off-campus facilities Student tuition Subawards (amount above the first $25,000 of each subaward)

Equipment is defined as an article of non-expendable tangible personal property having a useful life of more than two years, and an acquisition cost of $5,000 or more.

Calculate Indirect Cost by multiplying total direct cost by the appropriate indirect cost rate. No items are excluded from the Indirect Cost calculation for non-federal Grants and contracts.

Director, Non-Federal Audits Office of Inspector General U.S. Department of Education Wanamaker Building 100 Penn Square East, Suite 502 Philadelphia, PA 19107 Phone: (215) 656-6900

U.S. Department of Health & Human Services Mr. Arif Karim Branch Chief–Colleges & Universities, Hospitals and Nonprofit Organizations Cohen Building, Room 1067 330 Independence Avenue, SW Washington, DC 20201 Date Disclosure Statement was filed: 03/12/2015

For additional information, please refer to the new Guidance on Salary Limitation for Grants and Cooperative Agreements from March 01, 2023 NOT-OD-22-076 (new window)